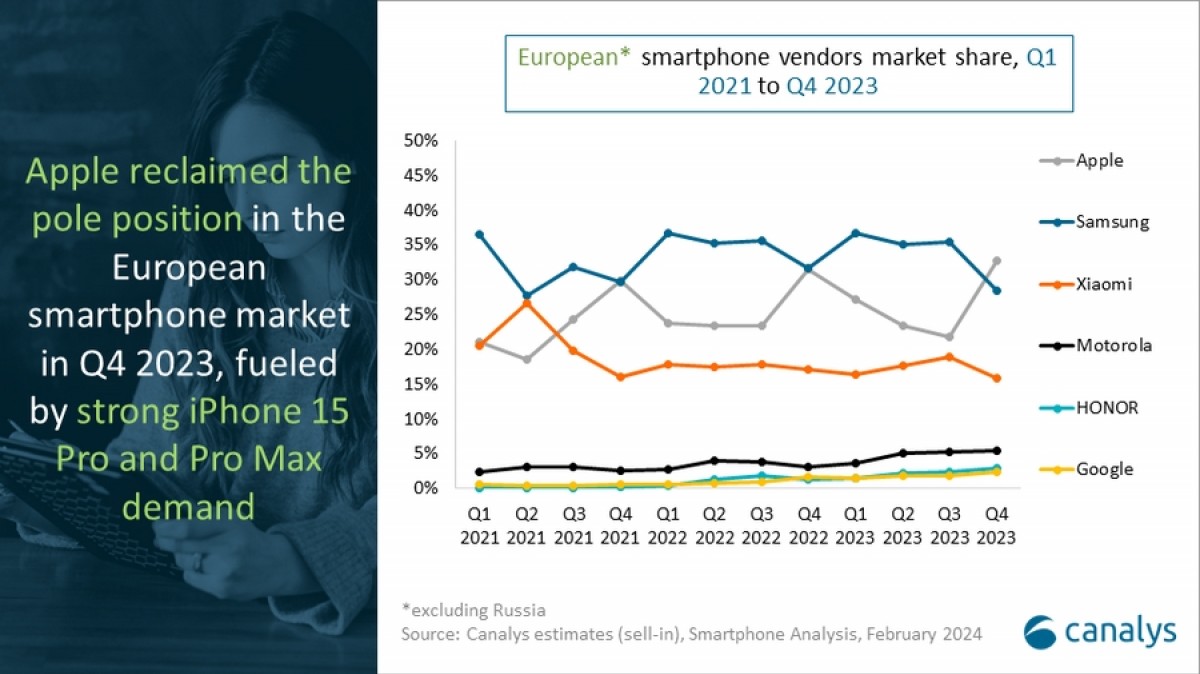

Canalys revealed that Apple became the best-selling smartphone maker in Europe during Q4 2023. The US company’s success was fueled by strong demand for the iPhone 15 Pro and Pro Max during the holiday period, but Samsung kept the top spot for the whole of 2023.

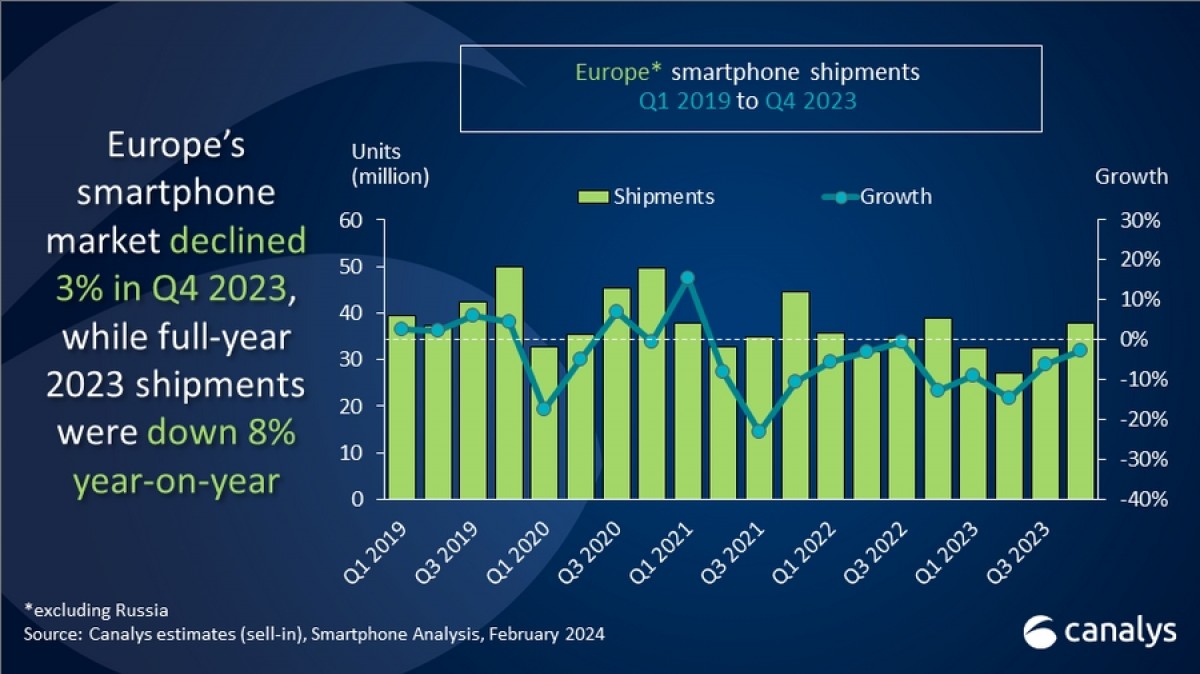

The overall market saw 129.8 million shipments for the calendar year, which was 8% lower than the 140.8 million units in 2022. However, Canalys predicted that Europe will see a single-digit growth next year, driven by an impending refresh cycle of devices bought during the pandemic.

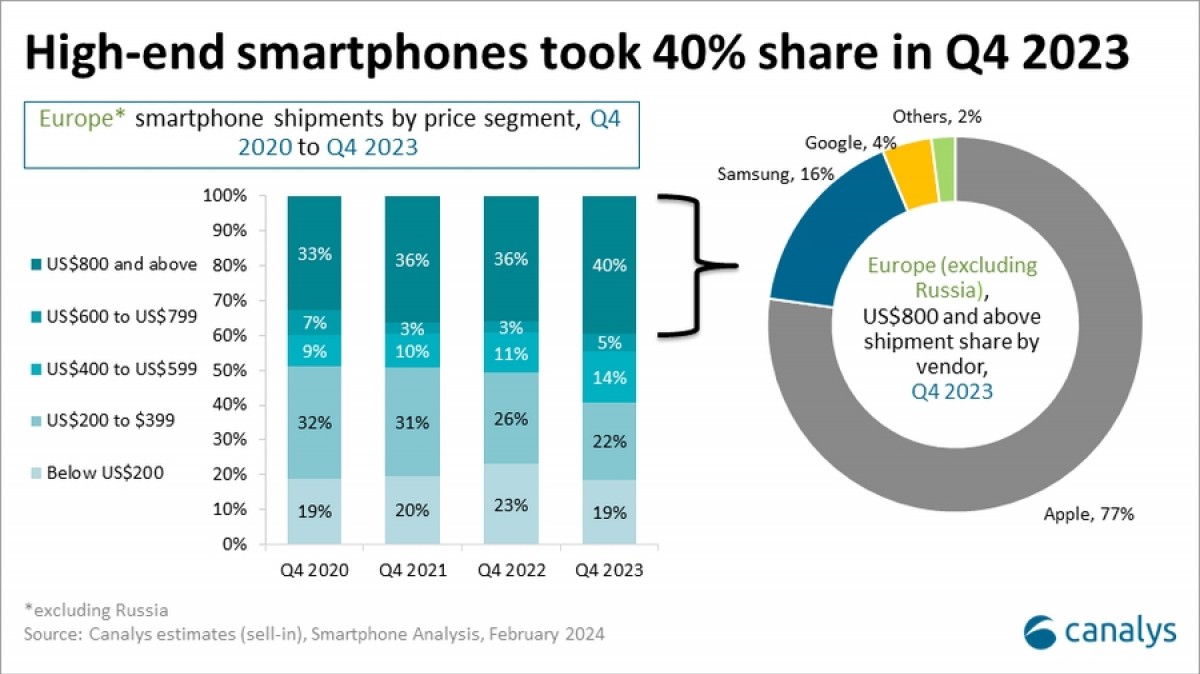

High-end smartphones took a record share of the whole European market in Q4 2023. According to Runar Bjorhovde, Analyst at Canalys, almost 40% of all shipments were for phones that cost over $800. Three out of four devices were an iPhone, followed by Samsung with a mere 16% share.

Apple kept a nearly flat amount of shipments during Q4 2023; it is Samsung and Xiaomi that flopped massively, allowing the US company to rise on top. The Top 5 saw the resurgence of Honor, and Canalys said we should expect smaller brands to increase their share in the near future. This includes Oppo, which settled with Nokia on 5G patents, allowing the Chinese maker to reintroduce its devices in major European markets.

| Company | Q4 2023 shipments (in million) |

Q4 2023 market share |

Q4 2022 shipments (in million) |

Q4 2022 market share |

Change |

| Apple | 12.4 | 33% | 12.2 | 31% | 1% |

| Samsung | 10.8 | 28% | 12.3 | 32% | -12% |

| Xiaomi | 6.0 | 16% | 6.6 | 17% | -10% |

| Motorola | 2.0 | 5% | 1.2 | 3% | 73% |

| Honor | 1.1 | 3% | 0.5 | 1% | 116% |

| Others | 5.5 | 15% | 6.1 | 16% | -8% |

| Total | 37.8 | 100% | 38.9 | 100% | -3% |

Companies would see an increase in shipments only if they apply a holistic approach emphasizing innovation, reliability, backend logistics, regulatory compliance, and a clear brand message, added Bjorhovde.

| Company | 2023 shipments (in million) |

2023 market share |

2022 shipments (in million) |

2022 market share |

Change |

| Samsung | 43.7 | 34% | 48.9 | 35% | -11% |

| Apple | 34.6 | 27% | 36.2 | 26% | -4% |

| Xiaomi | 22.2 | 17% | 24.7 | 18% | -10% |

| Motorola | 6.4 | 5% | 4.7 | 3% | 34% |

| Oppo | 3.7 | 3% | 6.7 | 5% | -45% |

| Others | 19.2 | 15% | 19.6 | 14% | -2% |

| Total | 129.8 | 100% | 140.8 | 100% | -8% |

In the long run, vendors will increase focus on the on-device user experience with AI at the core, emphasizing personalization, ecosystem interaction, productivity, and entertainment. However, investing in AI should be followed by educating consumers on maximizing the power of on-device AI features; otherwise companies might not see a strong return on their investment.