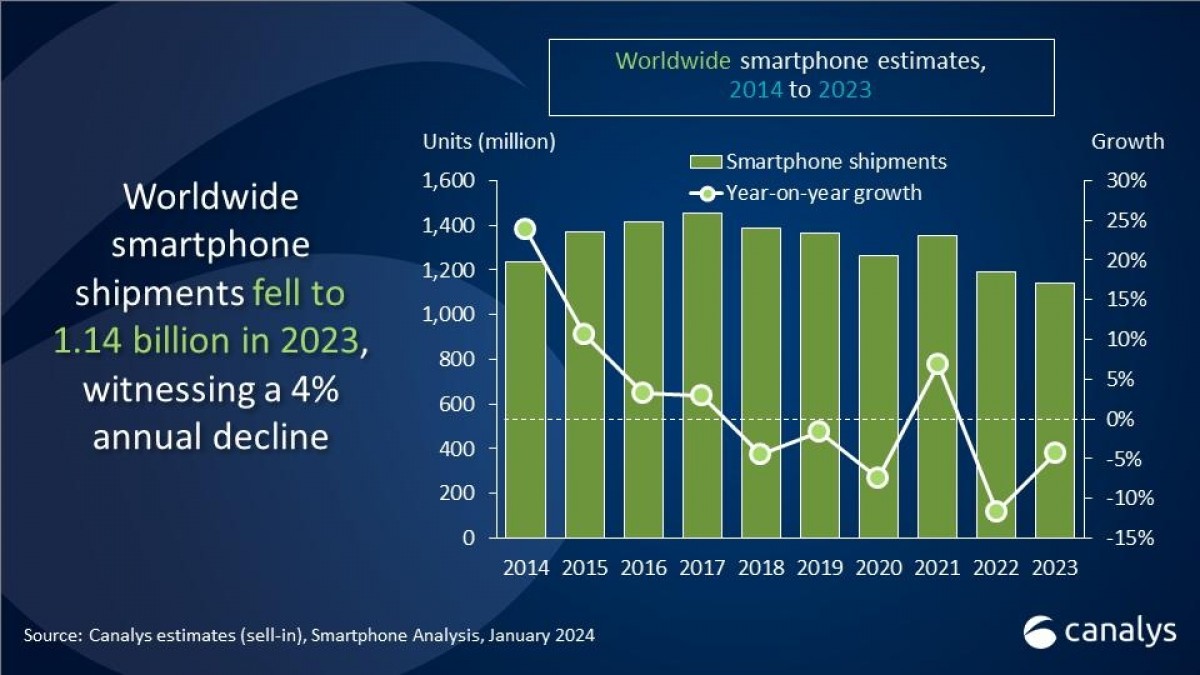

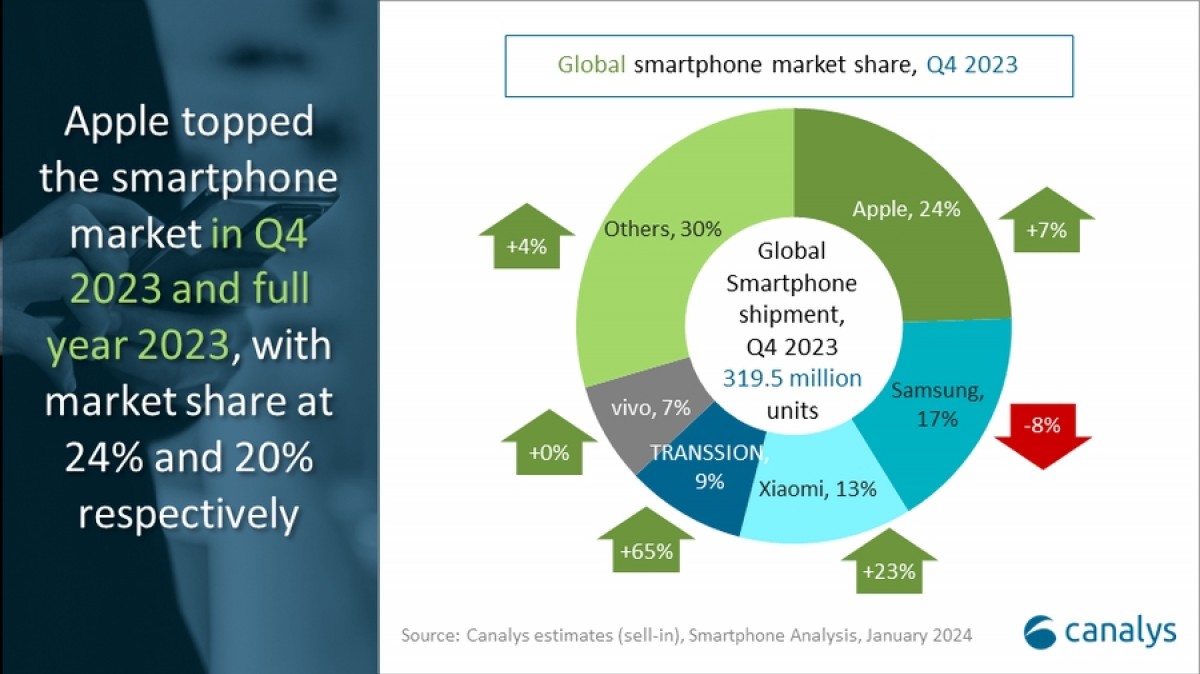

Smartphone shipments in 2023 totaled 1.142 billion – the worst in 11 years, claims Canalys in its latest analysis of the market. Apple took the top spot for the first time on the back of a stagnant year in which its main competitor, Samsung, declined 13%.

The holiday period was a positive one for the industry, with an 8% increase, which is a sign of stabilization, according to the analysts.

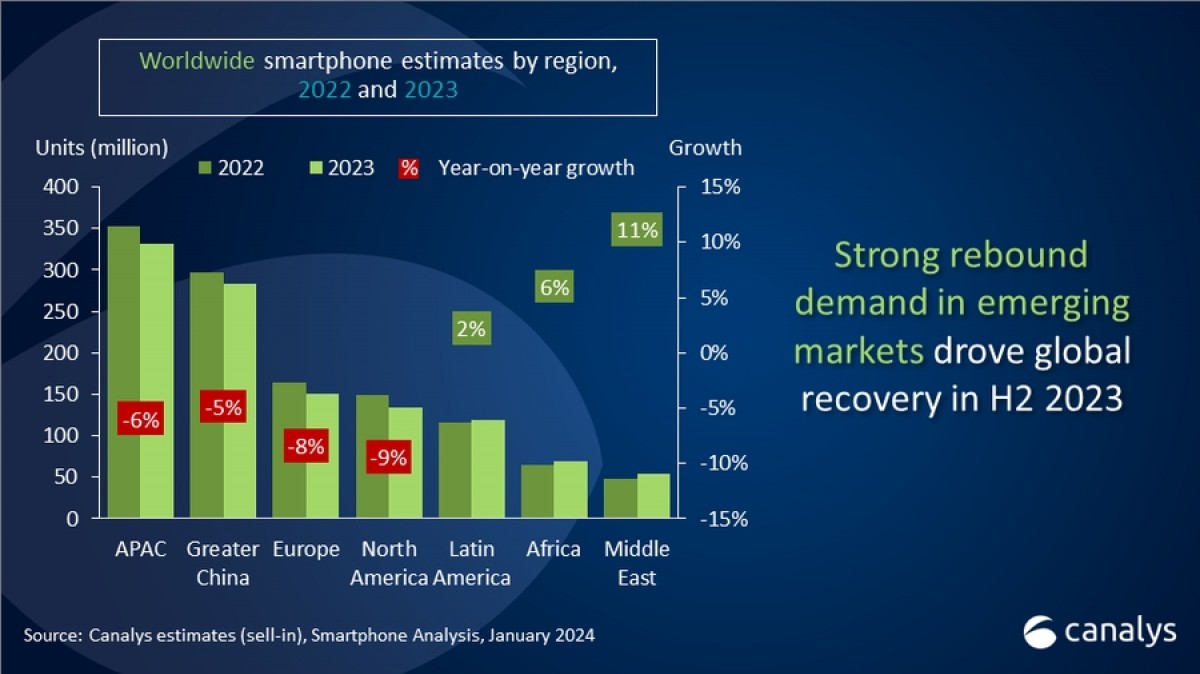

The smartphone market experienced serious headwinds, but rebounding demand in emerging markets drove global recovery in the second half of the year, commented Sanyam Chaurasia, Senior Analyst at Canalys. Latin America, Africa and the Middle East actually saw a YoY growth in shipments, largely offsetting the decline in the rest of the world (Asia Pacific, Mainland China, Europe, and North America).

Transsion (owner of iTel, Infinix, and Tecno) and Xiaomi have benefited from the rebound, achieving a remarkable increase during the October-December 2023 period. The increase in demand pushed Transsion to fourth place for Q4 2023.

The emerging markets will remain a vital battleground for all makers, seeking growth as developed regions such as North America and Europe are facing subdued consumer spending and reduced channel investments.

The market did decline, but the inventory backlog is no longer a major issue, and the low prices of components should allow vendors to support more flexible incentive measures to consumers.

| Company | Q4 ’23 shipments (million) | Q4 ’23 Market share | Q4 ’22 shipments (million) | Q4 ’22 Market share | Change |

| Apple | 78.1 | 24% | 73.2 | 25% | 7% |

| Samsung | 53.5 | 17% | 58.3 | 20% | -8% |

| Xiaomi | 41.0 | 13% | 33.2 | 11% | 23% |

| Transsion | 28.5 | 9% | 17.3 | 6% | 65% |

| vivo | 23.9 | 7% | 23.9 | 8% | 0% |

| Others | 94.4 | 30% | 90.9 | 31% | 4% |

| Total | 319.5 | 100% | 296.9 | 100% | 8% |

Looking at the raw numbers, Apple and Samsung remain the market leaders globally, followed by Xiaomi in third and Oppo in fourth. Companies like vivo and Honor released their flagships and are expected to challenge Transsion for a place in the Top 5.

| Company | 2023 shipments (million) | 2023 Market share | 2022 shipments (million) | 2022 Market share | Change |

| Apple | 229.2 | 20% | 232.2 | 19% | -1% |

| Samsung | 225.4 | 20% | 257.9 | 22% | -13% |

| Xiaomi | 146.4 | 13% | 152.7 | 13% | -4% |

| Oppo | 100.7 | 9% | 113.4 | 10% | -11% |

| Transsion | 92.6 | 8% | 73.1 | 6% | 27% |

| Others | 347.9 | 30% | 364.1 | 31% | -4% |

| Total | 1142.1 | 100% | 296.9 | 100% | -4% |

The year 2024 should see makers go in two strategic directions – either investing in on-device AI or expanding shipments in the mid-to-low-end segment. Samsung just released its Galaxy S24 smartphones with Galaxy AI globally, while Chinese companies launched the phones on the domestic market; surely, the next step will be expanding internationally.

The mass-market segment will be the center for vendors, while value-for-money proposition and affordability are core product strategies in the short term, added Zhu.