Advanced Micro Devices (NASDAQ: AMD) stock price hit a 52-week high on March 8, but shares of the chipmaker have pulled back more than 15% since then, even though there has been no notable company-specific development in the interim.

Of course, reports that China is reportedly planning to replace chips made by AMD and Intel from Chinese government servers and personal computers (PCs) did weigh briefly on the stock price, but even that shouldn’t be a big problem for AMD in the long run. Here’s why.

Sanctions in China shouldn’t be much of a trouble for AMD

AMD reportedly gets 15% of its total revenue from selling its chips to China. So, any sanctions on sales of its chips in that country may have an impact on AMD’s financials. However, the dynamics of the semiconductor market are such that even if AMD is unable to sell its chips in China, it will have other avenues to sell them.

For instance, sales of both servers and PCs are expected to grow strongly across the globe thanks to the adoption of artificial intelligence (AI). Sales of PCs fell just 2.7% year over year in the fourth quarter of 2023 as compared to the 14% drop for the entire year. The market is set to witness a turnaround in 2024, driven by a new refresh cycle in the enterprise and education markets, as well as the arrival of AI-enabled PCs.

Market research firm Canalys estimates that 48 million AI PCs could be shipped this year, accounting for 18% of the overall market. What’s more, shipments of AI PCs could grow at an annual rate of 44% through 2028 and account for 70% of the overall market. Canalys also points out that AI PCs are likely to command a 10% to 15% premium as compared to traditional machines.

AMD, therefore, has an opportunity to boost both its volumes and average selling price (ASP) of central processing units (CPUs). It is also worth noting that AMD has been taking share from Intel in the PC market. The company controlled 20.2% of the client CPU market in the fourth quarter of 2023, up from 17.1% in the year-ago period, as per Mercury Research.

Mercury Research attributed the share gains to AMD’s early move into the market for AI PCs with its Ryzen 7040 processor. Meanwhile, AMD claims that its CPUs are powering over 90% of AI PCs currently in the market. So, the stronger demand for AI PCs is going to give AMD’s client processor business a nice shot in the arm.

Something similar is likely to unfold in the server CPU and GPU (graphics processing unit) markets. AMD finished 2023 with 23% of the server CPU market under its control, up from 17.6% in the year-ago period. AMD CEO Lisa Su remarked on the latest earnings conference call that the company is witnessing “robust demand for EPYC server CPUs across cloud, enterprise, and AI customers.”

AMD also added that “a growing number of customers are adopting EPYC CPUs for inferencing workloads.” The good part is that AMD’s server CPU momentum is here to stay, as the market for AI servers is predicted to clock 26% annual growth through 2029. On the other hand, AMD saw stronger-than-expected demand for its AI GPUs as well.

AMD increased its full-year revenue forecast from data center GPUs to $3.5 billion from the earlier estimate of $2 billion. However, management made it clear on the earnings call that it could very well exceed that mark because of an improving supply chain that will help it meet additional demand. All this indicates that AMD is well-placed to trump analysts’ expectations in the coming quarters.

AMD could surprise investors with stronger-than-expected growth

When AMD released fourth-quarter 2023 results on Jan. 30, 2024, the company guided for $5.4 billion in revenue for the first quarter of 2024 at the midpoint. That would be nearly flat from the prior-year period’s revenue of $5.35 billion. Additionally, AMD’s non-GAAP (generally accepted accounting principles) gross margin guidance of 52% for the current quarter would be a slight improvement over the year-ago quarter’s reading of 50%.

AMD’s revenue and earnings, therefore, could increase slightly in Q1. Analysts, however, expect AMD to post $5 billion in quarterly revenue, which is lower than what the company has guided for. Additionally, consensus estimates forecast a decline in AMD’s earnings to $0.55 per share from $0.60 per share in the year-ago period.

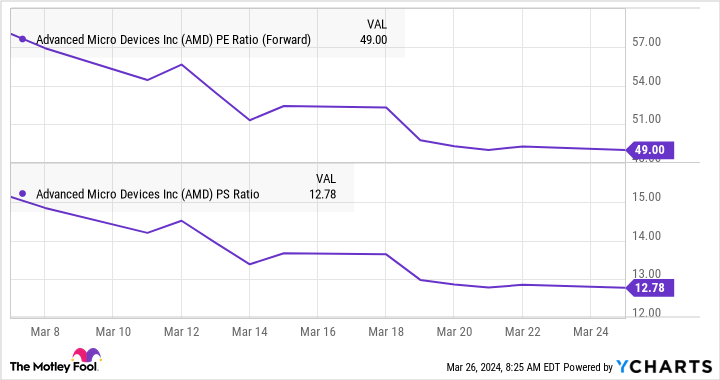

However, there is a solid chance that AMD could beat the market’s expectations by a big margin because of the multiple AI-related tailwinds discussed above. The good part is that AMD’s pullback has made the stock cheaper than before. This is evident from the chart:

AMD is now trading at 49 times forward earnings and has a price-to-sales ratio of less than 13. It was trading at more than 57 times forward earnings and 15 times sales earlier this month. Savvy investors can consider using this drop to accumulate AMD stock as the above-mentioned growth drivers could help it regain its mojo, and the turnaround could begin as soon as next month when it releases its first-quarter 2024 results.

Should you invest $1,000 in Advanced Micro Devices right now?

Before you buy stock in Advanced Micro Devices, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Advanced Micro Devices wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices. The Motley Fool recommends Intel and recommends the following options: long January 2023 $57.50 calls on Intel, long January 2025 $45 calls on Intel, and short May 2024 $47 calls on Intel. The Motley Fool has a disclosure policy.

AMD Stock Is Down 15% From Its 52-Week Highs, and Here’s Why You Should Buy It was originally published by The Motley Fool